- Telephone

- Email

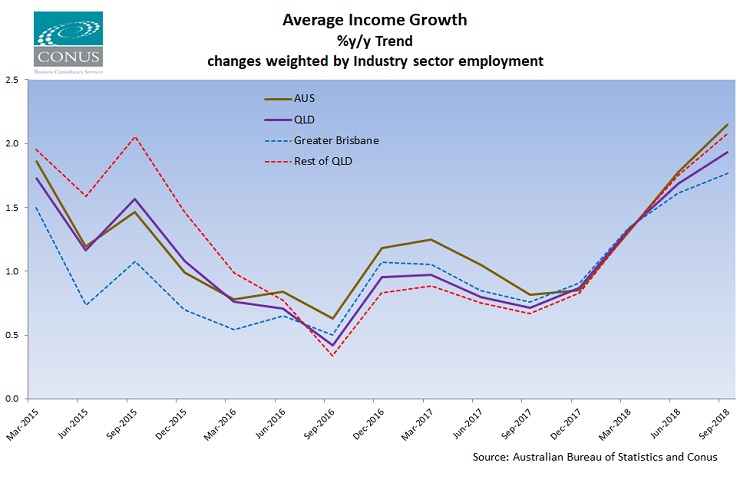

Last month saw the release of the Labour Account series which provided details of income growth rates for various industry sectors (see here for our post at the time). Given the various income growth rates across industry sectors and combining this with the industry employment breakdown at the regional level (from our own Conus Industry Employment Trend data; see here for details) we can estimate income growth rates across the various SA4 regions in Queensland*. Doing so provides us with some interesting insights.

While average income growth across the nation (weighted by industry sector employment) was 2.15%, Queensland saw an increase of just 1.93%. Digging deeper into the state data we see that Greater Brisbane achieved income growth of just 1.77% while the Rest of Queensland manged a more impressive 2.08%. The main reasons for the differences can be summarised as;

Within a few specific regions we saw (data for additional regions is available…please contact us for details);

| Average Income y/y Sept 2018 | |

| Australia | 2.15 |

| Queensland | 1.93 |

| Greater Brisbane | 1.77 |

| Brisbane – East | 1.73 |

| Brisbane – North | 1.50 |

| Brisbane – South | 1.67 |

| Brisbane – West | 1.48 |

| Brisbane Inner City | 1.20 |

| Ipswich | 2.22 |

| Logan – Beaudesert | 2.37 |

| Moreton Bay – North | 1.99 |

| Moreton Bay – South | 1.64 |

| Rest of Qld | 2.08 |

| Cairns | 2.45 |

| Darling Downs – Maranoa | 2.39 |

| Fitzroy | 2.67 |

| Gold Coast | 1.92 |

| Mackay | 2.01 |

| Qld – Outback | 1.67 |

| Sunshine Coast | 1.52 |

| Toowoomba | 1.80 |

| Townsville | 2.26 |

| Wide Bay | 2.49 |

*Notes on the data

The data set is derived using the quarterly average income per employed person data from the ABS Labour Account (6150.0.55.003).

At the industry level the yearly average income changes are then weighted by the percentage of total employment in each industry sector as calculated from the Conus Industry Jobs Trend series (which is in turn derived from the original ABS Labour Force Detailed Quarterly data set; 6291.0.55.003) for State and Region, and from the ABS Trend Persons Employed data in the Labour Account for Australia.

The resulting data therefore gives an indication, at the regional level, of the average income change.

The Labour Account average income data is for quarters ending in March, June, Sept and Dec whereas the Labour Force Detailed Quarterly is for quarters ending in Feb, May, Aug and Nov. Nevertheless, the difference (particularly when seen on a Trend basis) of this timing issue is likely to be minimal.

Actual income data at the regional level is not available. Therefore, the derived changes assume that income changes across industry sectors are common across regions. Differences across regions in average incomes are due to variations in the industry make-up of the employment in those regions.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series