- Telephone

- Email

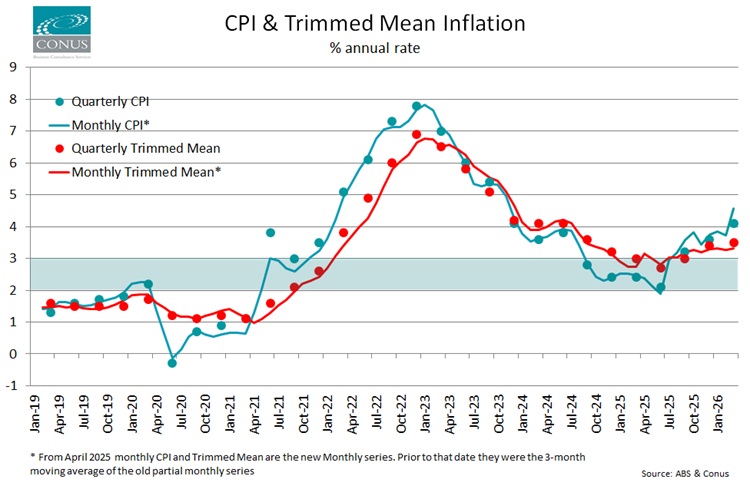

Last week’s March quarter CPI release threw up two different stories depending on which line you read. The new monthly CPI Indicator had the Trimmed Mean unchanged at 3.3% over the year to March. The quarterly series, still published as an appendix to the main release and the measure the RBA has been leaning on, had the Trimmed Mean rising to 3.5% in Q1, up from 3.4% in Q4 last year. The headline measures differed too: monthly indicator at 4.6%, quarterly series at 4.1%. Same data; different methodology; very different signal.

The gap between the two readings is methodological, not a typo. The ABS only moved to a complete monthly CPI series late in 2025 and the seasonal adjustment of the new monthly Trimmed Mean is still settling. The RBA has been explicit, in both November’s SOMP and February’s, that until those seasonal patterns are nailed down it is treating the quarterly Trimmed Mean as the primary underlying signal. The monthly indicator is a useful cross-check, not the lead measure. So the line that should be in the Board’s papers tomorrow is the 3.5%, not the 3.3%.

That 3.5% matters because of where it sits on the curve. The quarterly Trimmed Mean troughed at 2.7% in the June quarter of 2025, the closest the series has been to the middle of the RBA’s 2-3% target band in this cycle. Since then it has gone 3.0%, 3.4% and now 3.5%. Three consecutive quarters of acceleration after a clean disinflation through 2024. Headline quarterly CPI tells the same story, troughing at 2.1% in Q2 2025 and now back to 4.1%. The disinflation has not just stalled, it has reversed.

Some of that is supply-side noise the RBA will look through. Automotive fuel spiked 32.8% in March on the back of Middle East-driven oil prices, and electricity is 25.4% higher than a year ago as Commonwealth and State rebates have rolled off. The Trimmed Mean is built precisely to strip that volatility out, which is why a rising Trimmed Mean is the more uncomfortable read. It says the underlying pressure is broadening, not just energy and rebates. Housing at 6.5% y/y is doing some of that work.

The implication is the same one mortgage holders have been wearing since February’s hike. With the cash rate at 4.10%, the quarterly Trimmed Mean now at 3.5% and trending the wrong way, and ASX 30-day futures pricing roughly an 86% probability of a 25 basis point hike tomorrow, the case for the RBA to keep moving is uncomfortably clear. We will know by 2:30pm Tuesday.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series