- Telephone

- Email

Buried in the Statement on Monetary Policy released last week is an ‘In Depth’ chapter on the impact of higher global energy prices on the Australian economy. It is worth reading on its own merits, but it is worth reading with one specific question in mind: what does this mean for Far North Queensland? The short answer is that the RBA is describing the FNQ economy without quite naming it.

The big numbers first. Headline inflation jumped to 4.6% in the year to March from 3.7% in February, with fuel prices up 32.8% in the month, the largest single-month increase since the monthly CPI series began in 2017. Fuel contributed 0.8 ppts of that headline jump on its own. The RBA’s rule of thumb is that a 10% rise in domestic fuel prices flows through to roughly 0.3 ppts of additional headline inflation over one to two quarters, and another 0.2 to 0.25% in the broader price level over one to two years as it works through input costs. We are well past the 10% mark.

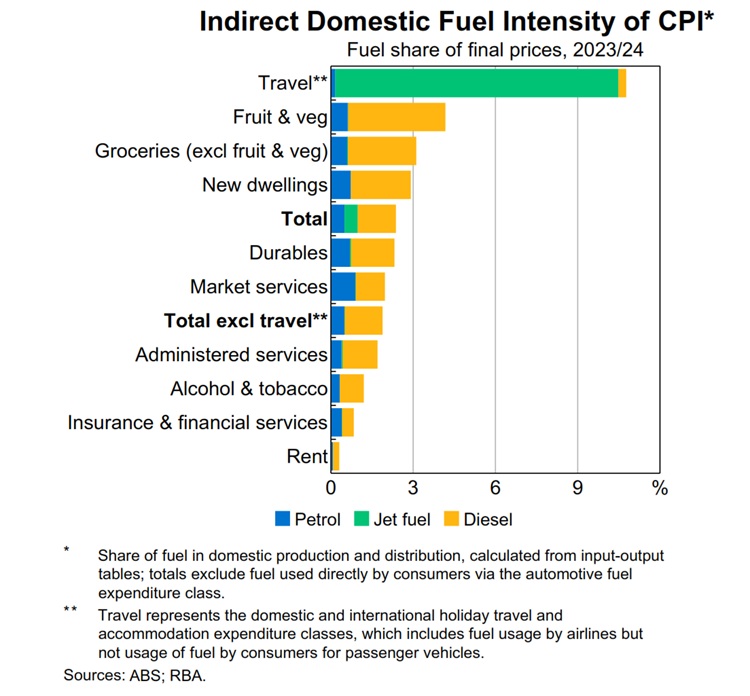

The In Depth chapter spells out three transmission channels that hit FNQ harder than the national average. The first is travel. The RBA notes explicitly that “holiday travel is heavily reliant on jet fuel, and so travel prices may be most sensitive to higher fuel costs.” TNQ’s economy is anchored by inbound holiday travel, much of it via Cairns Airport, and any sustained jet-fuel pass-through to airfares and package prices will land on tourism operators here before it lands on capital-city CBDs.

The second is road freight and the input cost of food. The RBA explicitly names fruit and vegetables, groceries and new dwelling construction as having higher-than-average shares of fuel costs in their domestic production and distribution. FNQ sits at the end of long supply lines for everything that does not grow or get built locally, and the Tablelands and Cassowary Coast cane, banana and beef operations are themselves heavy diesel users. About 90% of Australia’s diesel consumption is by businesses, with transport, mining and agriculture the largest users, a mix that describes FNQ’s productive base reasonably well.

The third is the household-side incidence. The RBA observes that cost pressures from higher fuel “would likely fall disproportionately on lower income households, which tend to spend a larger share of their income on petrol, and on those based in rural or regional areas needing to drive longer distances and with limited public transport options.” That is, almost word for word, a description of the FNQ household sector: lower median incomes than the metro average, longer travel distances, and limited public transport outside central Cairns.

None of this changes the cash rate, which is now 4.35% with market pricing implying 4.70% by year-end. But it does explain why the RBA’s own forecasts have GDP growth slowing to 1.3% by December 2026 while the unemployment rate edges out to 4.7% by mid-2028. A fuel-driven cost-of-living squeeze, layered on top of a tightening cycle, is not an FNQ-specific problem. It does, however, hit FNQ in a more concentrated way than it hits most of the country.

Chart from the May 2026 SoMP

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series