- Telephone

- Email

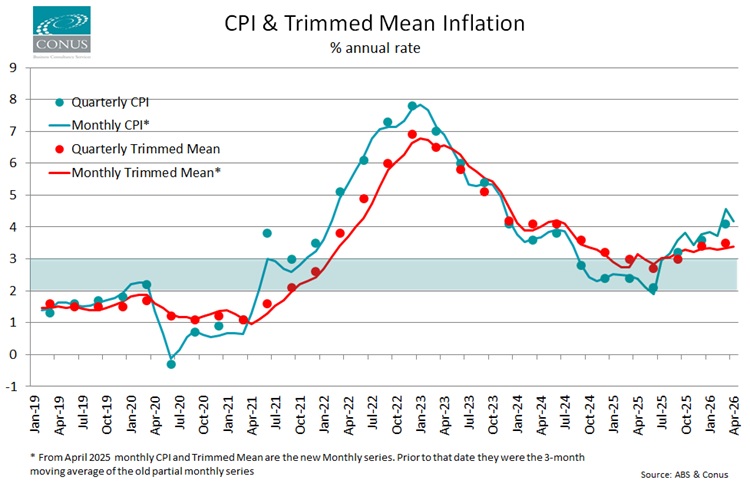

The headline monthly CPI Indicator for April came in at 4.2% y/y with a monthly rise of just 0.4% (after 1.1% in March), a touch softer than the market had been looking for (around 4.4%). The bulk of the easing came through Transport, which fell 2.7% m/m after rocketing 9.2% in March, as some of the worst of the war-driven fuel price pressures unwound.

As we always note, however, the headline is the noise and the Trimmed Mean is the signal. The monthly Trimmed Mean ticked up to 3.4% y/y (from 3.3% in March), broadly in line with what the market expected as some of the broader pass-through from higher fuel prices begins to feed into the wider basket. With the RBA still flagging that its preferred read is the older quarterly Trimmed Mean (which printed at 3.5% for the March quarter) rather than the new monthly series, an April monthly print this close to expectations is unlikely to shift the dial at the Board’s next meeting on 16 June.

The bigger picture has not changed. Even if the situation in Iran were to be resolved tomorrow (and that looks unlikely), the second-round effects of the fuel shock will be working their way through the economy for some time. The RBA has been clear and consistent throughout this cycle that its primary concern is ensuring inflation expectations do not become baked into wage and price setting decisions, and an April print that is down on March but with the underlying measure still drifting higher does not materially undermine the case for caution.

That said, price stability is not the RBA’s only mandate. The softer than expected seasonally adjusted employment data published last week has seen the futures market trim its hawkishness a notch. The ASX 30-day interbank cash rate futures are now pricing one more 25bp hike to a terminal 4.6% in the final quarter of 2026, with rates then on hold well into 2027.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series