- Telephone

- Email

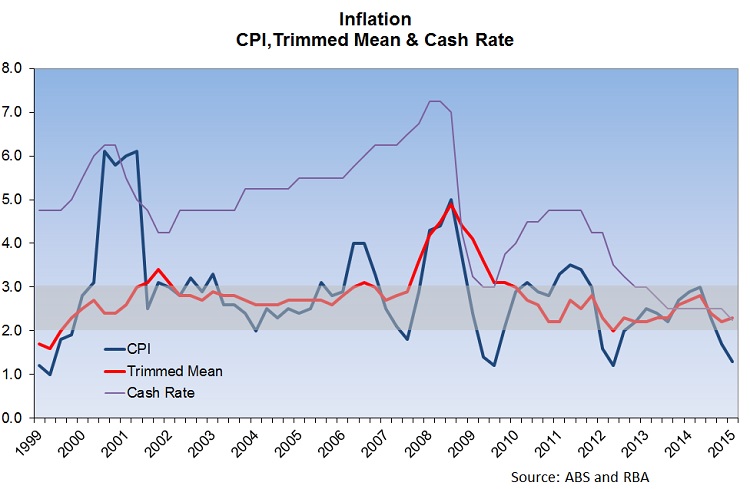

The headline inflation measure (Consumer Price Index, CPI) for the second quarter has come in bang-on market expectations at +0.2% q/q for a 1.3% increase over the year. The increase comes courtesy of a 2.6% yr/yr increase in non-tradables being offset by a 0.9% yr/yr fall in tradables.

The more closely watched (at least by the RBA and all those who care about the future direction of interest rates) measures of core inflation were marginally higher than expected. Trimmed Mean was +0.6% q/q, +2.3% yr/yr while the Weighted Median also rose 0.6% q/q for a 2.4% yr/yr gain. These slightly higher numbers, which see core inflation sitting just below the middle of the RBA’s 2-3% target range, led to a US 0.4 cent rise in the A$ and a decline in the market’s pricing for a May Cash Rate cut from about 52% to 44% at the time of writing. The graph below highlights the current divergence between CPI and core inflation measures. These periods of divergence are not unusual, but perhaps make the need to keep our eyes on the core measure clearer.

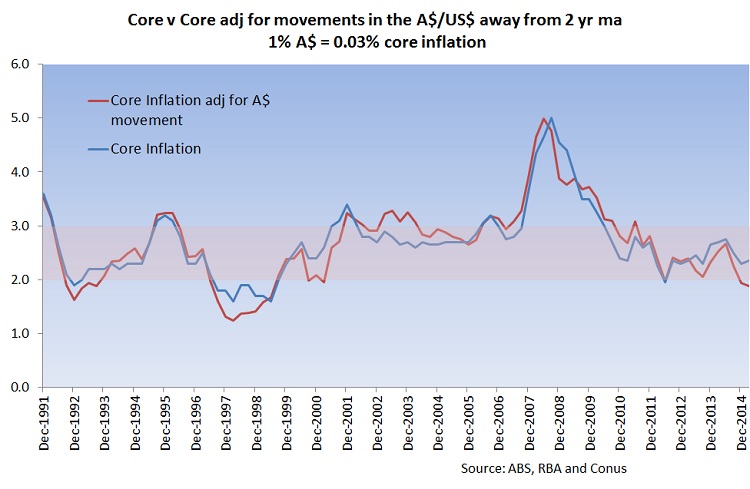

The variation in the tradable and non-tradable rates of inflation highlight the impact that the value of the A$ can have on headline inflation. The general rule of thumb has been that a 1% appreciation in the value of the A$ subtracts about 0.03% from core inflation (and vice-versa). In the graph below we have used deviation of the A$ value from a 2 year (8 quarter) moving average to calculate the “adjusted” core inflation figure. What we see is that the core inflation adjusted for the current weakness of the A$ below its 2 year moving average has moved below the 2% bottom of the RBA target; were it not for a weaker A$ adding to import price inflation we would probably be looking at core inflation below 2%.

Note that, despite tradables prices showing a 0.9% decline on the year, this measure is NOT a core figure and therefore incorporates some highly volatile import goods (notable petrol) which have fallen sharply; were it not for the weakness in the A$ we could have expected tradables inflation to have been even more negative.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series