- Telephone

- Email

Third quarter inflation has fallen, broadly in line with market expectations. The headline CPI rose 0.5% q/q for an annual increase of 2.3% (down from 3.0% in the June quarter). The RBA will be paying particular attention to the two “core” inflation measures. Trimmed mean rose 0.4% q/q and +2.5% y/y (after some small downward revisions to previous quarters), while Weighted Median rose 0.6% q/q and +2.6% y/y. The average of the two “core” measures shows inflation up 0.5% for the quarter (down from +0.65% in the previous quarter) and up 2.55% for the year (down from +2.7% in the previous quarter).

With the sharp declines seen in the A$ earlier in the year having slowed somewhat more recently we see the tradables (basically imported goods) inflation measure up just 2.0% for the year, down from a 2.9% rate last quarter. Of more interest (and no doubt of some concern to those talking of the fears of deflation) is the fact that non-tradables inflation rose just 2.4% for the year to Sept 2014. This is the slowest pace of non-tradables inflation since Sept 2009, when the economy was still reeling from the impacts of the GFC.

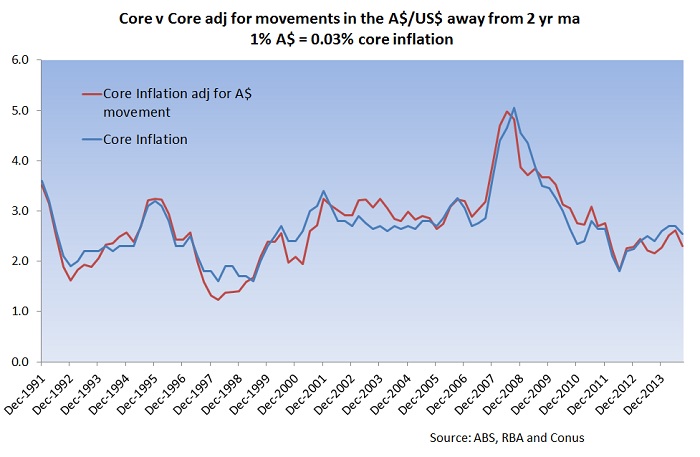

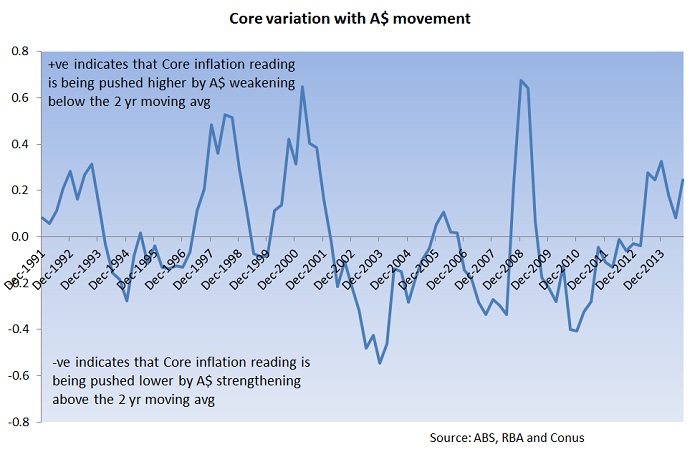

Previous studies have suggested that a 1% shift in the value of the A$ equates to approximately a 0.03% move in core inflation. The graph below shows average core inflation plotted with adjusted core inflation (adjusted by an amount corresponding to the deviation of the A$/US$ rate from its 2 year moving average).

The second graph plots the deviation between the two. Readings above zero indicate that core inflation is being pushed higher by a generally weakening A$ (and its corresponding upward pressure on import prices) ,while readings below zero indicate that the A$ is stronger than its 2 year moving average and therefore suppressing core inflation. What we see is that the weakness seen in the A$ over previous quarters is adding about 0.2% to core inflation. If we expect the A$ to weaken further then we can expect to see that effect remain, and even increase. If, however, we see the A$ regaining strength then this would reverse out this upward pressure and could see core inflation falling to, or even below, the bottom of the RBA target range of 2-3%.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series