- Telephone

- Email

Today saw the release of the June quarter Wages Price Index, and it shows us growth in wages stuck at the (expected) annual rate of 2.1%. Quarterly growth lifted a touch from the previous quarter (again, as expected) to register a 0.6% increase. When considering the split across the private and public sectors we once again see the public sector leading the way with growth of 0.6% q/q and 2.4% y/y versus 0.5% q/q and 2.0% y/y for the private sector (all numbers seasonally adjusted).

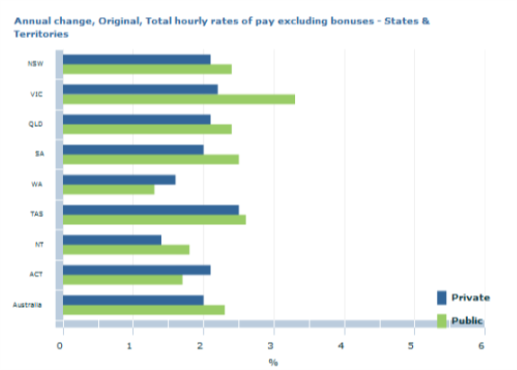

At the state level we must rely on the somewhat less reliable original data which shows QLD registered 0.4% q/q and 2.2% y/y growth. Across the sectors the year on year differential was similar to that at the national level with the private sector recording 0.4% q/q and 2.1% y/y while the public sector grew at 0.3%q/q and 2.4% y/y. As the chart below (sourced from the ABS website) shows, QLD public sector wages growth has actually been behind Victoria, SA and Tasmania, level with NSW but slightly faster than the national level (2.3% y/y original). Private sector growth is slightly better than the national average (2.0% y/y original) and beaten by just Victoria and Tasmania.

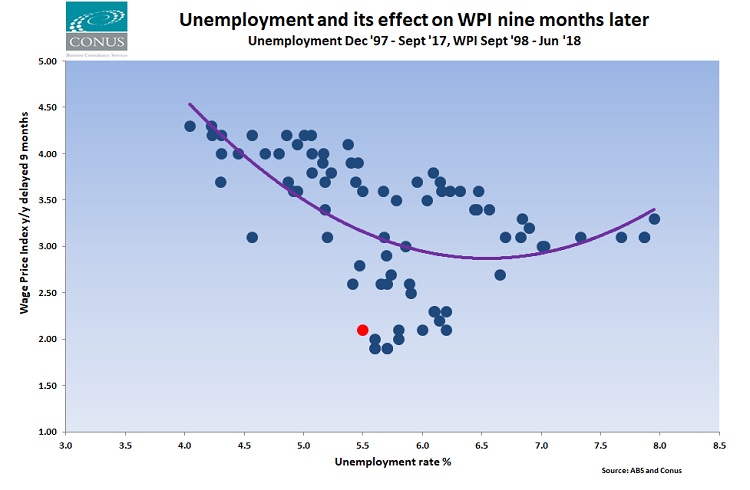

Tracking WPI against the unemployment rate provides us with some interesting observations. When we lag the WPI data by 9 months to compare (for example) Q2 2018 WPI with Q3 2017 unemployment to allow for the time it would take for labour shortages to impact on wages, we see that the current WPI reading is the lowest ever given an unemployment rate of 5.5% (as it was in Sept 2017) despite having crept slightly higher in the past year. It also demonstrates how far below historical trend levels we are.

We should also note that since Sept 2017 we have seen a very slow grind lower in the Trend unemployment rate so that it sat at 5.4% by June 2018. If we are not to see an even more exceptionally low WPI plot for the September 2018 data we must expect WPI to have shifted closer to 2.5% by then.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series