- Telephone

- Email

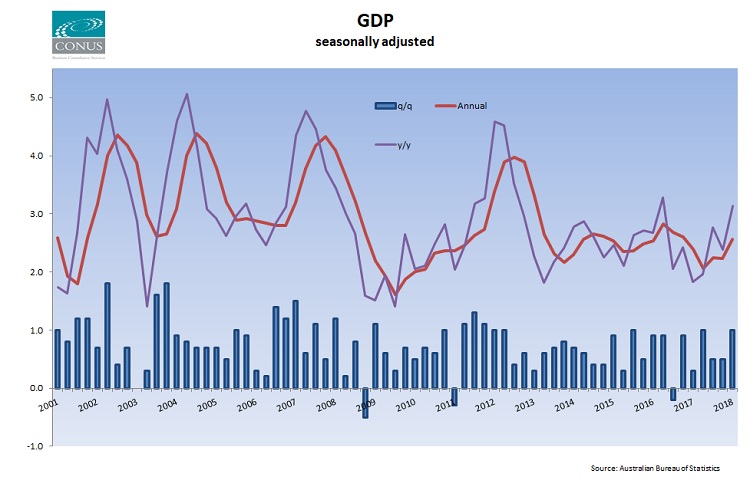

The GDP data for the first quarter has shown a sharp pick-up from last quarter and was somewhat higher than market expectations. On a seasonally adjusted basis GDP rose 1.0% for the quarter, or 3.1% from the same time a year ago. This brings the cumulative increase for the year to March to a 2.6% increase; up from 2.2% in the previous quarter, and the best result since the end of 2016.

The main contributor to growth this quarter was Net Exports, which added 0.4 ppts to growth, although positive contributions were also seen from inventories, household consumption, government consumption and private fixed investment.

Household savings continued to fall and the household savings ratio now sits at 2.1, its lowest level since the end of 2007. In the face of persistently weak wages growth (currently running at an annual rate of just over 2%) it is no surprise to see households running down savings to feed consumption; the question is how long can that continue to be sustainable? At some point we either need to see wages growth pick up to sustain the growth in consumer expenditure, or we are likely to see the household sector tightening the purse-strings once again. Certainly this quarter we saw a generally weak outcome from the household sector with consumption increasing just 0.3% for the quarter (the equal lowest pace of growth in 5 years).

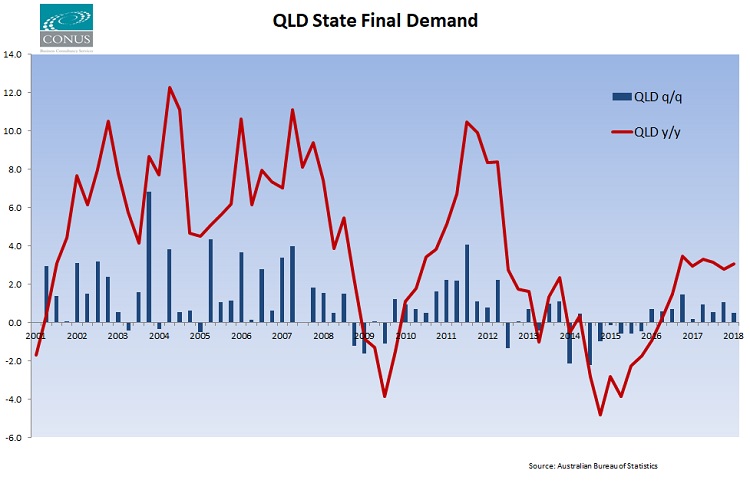

In Queensland we see State Final Demand (which does not include the State’s strong export sector) up 0.5% q/q (after the Q4 data was revised up a little to +1.1%). Year on year growth is now running at +3.1%, up from 2.8% last quarter. Annual growth now sits at 3.1% for the year to March 2018 after a rate of 3.2% for the previous quarter (after upward revisions).

In Trend terms State Final Demand rose 0.7% q/q and, as the chart below shows, is being kept positive by a steady recovery in Public sector activity rather than anything else. The Private sector (incl consumption and investment) was up just 0.4% q/q while the Public sector lifted by 1.5%. As we noted last quarter, the recovery we had been seeing in Private sector investment appears to have now run out of steam.

The latest CONUS Quarterly is available for download below and includes an in-depth look at the Far North and Queensland economies.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series