- Telephone

- Email

Our good friend Graham Turner at GFC Economics in London has today released his quarterly Australia Economic Chartbook. It’s always interesting to see the way that such a respected economist from the other side of the world views our economy. The overview at the start of the Chartbook states…

Australia has weathered the impact of lower commodity prices, creating a significant number of new jobs in services. Strong investment in software has provided a boost, particularly for the financial services sector. Nevertheless, real spending on research & development (R&D) was only 1.04% of GDP in Q1 and is trending down. Australia faces similar long-term risks as the UK, where R&D expenditures are well below the OECD average.

However, the real trade balance is turning sharply higher: a deficit of AUD13.80bn in Q1 2012 has been turned into a surplus of AUD12.61bn in Q1 2016. The trade deficit in nominal terms should narrow more significantly in the second half of the year, in response to higher commodity prices. This may underpin further appreciation in the Australian Dollar.

Furthermore, the composition of exports is shifting rapidly towards services. The share of services exports has risen from a trough of 15.8% in December 2011 to 23.5% in April, the highest in eleven years. Australia is benefitting from stronger tourism (particularly from China) and exports related to information & communication.

Cooling the housing market remains a challenge. That said, the tighter lending restrictions implemented by the RBA are leaving their mark. Lending commitments for housing fell 13.3% y/y in April. Furthermore, residential construction has accelerated sharply over the past two years (+6.0% y/y in Q1), led by New South Wales (+21.1% y/y). The Government is responding to the housing shortage. House prices were still up 7.4% y/y in Q1, but could start to slow.

A deceleration in the housing market will weigh on growth in the short run. However, wages are picking up. In nominal terms, employee compensation accelerated to 3.6% y/y in Q1, the fastest increase since Q4 2012. In real terms, employee compensation rose 2.4% y/y. The acceleration partly reflects the rapid expansion in technology-related jobs, which are higher paid. Excluding manufacturing and mining, compensation jumped 4.5% y/y in Q1.

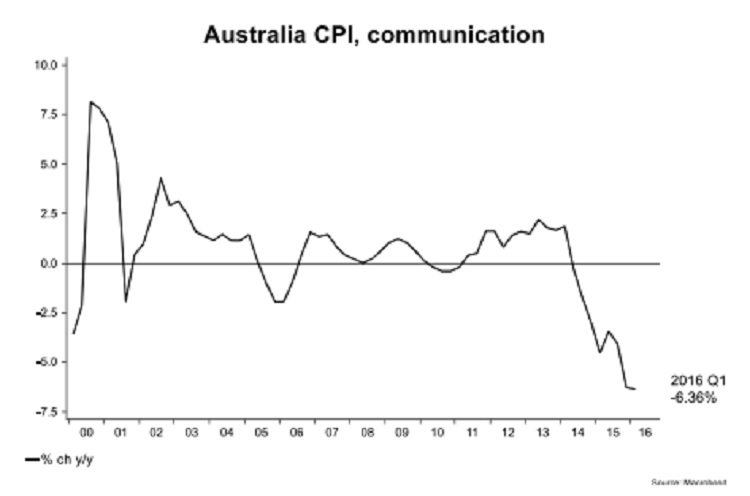

The pick-up in wages puts the weak CPI numbers into context. Low inflation partly reflects the impact of technology. The CPI for telecommunication equipment and services plunged 6.7% y/y in Q1. Inflation in ‘recreation & culture’ also slowed sharply (0.1%) due to a significant decline in audio, visual & computing equipment (-6.3%).

I’ve included one of Graham’s charts on telecommunication prices which highlights the point he makes.

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series

We are proud to have CBC Staff Selection as supporters of the Conus/CBC Staff Selection Trend Employment and Jobseeker data series